Opinion: Forget the fintech vs. bank battle —Africa’s financial future lies in unlikely alliances

With over 300 million people in Africa lacking access to basic financial services, Africa’s financial industry cannot afford to become embroiled in rivalries between traditional banks, fintech companies, microfinance institutions, and telecom giants.

By Bathsheba Asati, Principal Strategy Custodian, Amahoro Coalition, and Kwadwo Adjei-Barwuah, Head of Investment at Growth Investment Partners, Amahoro Coalition

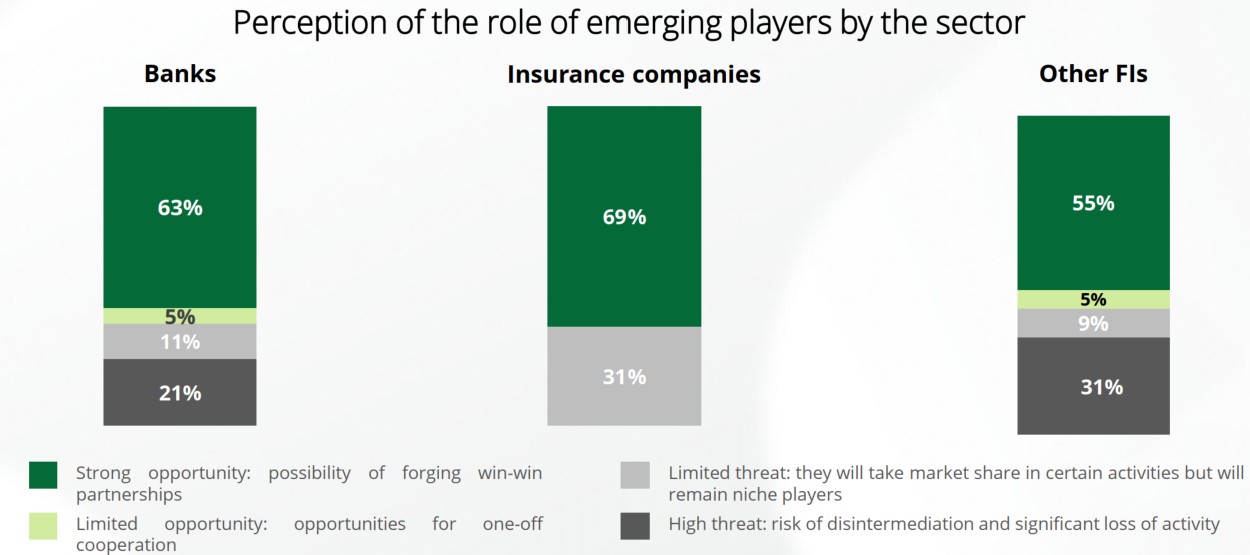

While many banks recognise the potential to collaborate with digital players, the latest AFIS-Deloitte Barometer reveals that 32% of bank respondents still view these firms as a competitive threat.

However, the future of financial services in Africa isn’t about whether traditional banks will become obsolete or if disrupters can sustain momentum.

Instead, real potential lies in forming strategic partnerships between these organisations and sharing insights to build products for the unbanked and underbanked that go beyond the payments sphere.

The industry ‘godfather’ will need to evolve

Banks have long been seen as the “Godfathers” of the industry, largely due to their role as custodians of trust and financial stability.

According to Uzoma Dozie, CEO of Nigerian fintech Sparkle (formerly CEO of Diamond Bank): “Banks have capital and the trust of their customers; any player looking to enter the financial industry needs to understand banking to offer a fuller breadth of services to their clients, beyond payment solutions.”

While banks occupy a pivotal role, they have no choice but to evolve alongside emerging players.

Fintech disrupters have challenged established business models

Fintech innovation has been at the forefront of expanding formal financial access for adults in Sub-Saharan Africa from 26% in 2011 to 57% in 2023.

And the fintech sector is projected to grow further, reaching a $65 billion valuation by 2030.

Mobile money platforms like M-Pesa, with 60 million users, exemplify how telecom giants have disrupted traditional banking, providing accessible and efficient alternatives.

Wave, now reaching 80% of Senegalese adults monthly, has also challenged the market with a 1% P2P fee—far lower than traditional rates—accelerating West Africa’s fintech boom.

Elsewhere, AI-powered services like Orange Money in Côte d’Ivoire can approve loans in just 10 seconds, while microfinance institutions have also expanded their reach, issuing approximately 50 million microloans to smallholder farmers and entrepreneurs.

While most banks see strong opportunities for partnerships with digital players in the next 3-5 years, 32% of bank respondents to the latest AFIS-Deloitte Barometer see digital actors as a threat

The partnership prospects beyond payments

Banks have an opportunity to leverage their trust and stability to partner with or learn from emerging players.

Joëlle Hazoume, Partnerships and Business Development Director at Orange Money, said: “Banks cannot compete with the network of a mobile operator or the agility of a fintech,” highlighting each entity’s unique strengths.

This sentiment reinforces the need for collaboration in realising a more inclusive financial landscape.

Financial inclusion is about more than onboarding customers

Achieving this requires a broader understanding of financial inclusion; it’s not merely about increasing the customer base. Rather, it’s about ensuring equitable access to a diverse array of financial services.

This means expanding beyond traditional payment services and creating pathways for underserved populations to access essential financial resources, tools, and education.

Partnerships between fintechs and traditional banks can lead to tailored products that cater to the unique needs of underserved populations – for instance mobile money providers can use their extensive customer bases to introduce users to banking products like savings accounts, credit options, and insurance coverage.

In Kenya, 45% of mobile money users have expressed interest in accessing microloans

through their mobile platforms, suggesting a significant opportunity for collaboration.

Omar Cisse, Managing Director and Founder of Intouch, said it is crucial for financial service providers to “keep the customer at the centre of it all, and provide these services sustainably not as a gift, but as value to their customers”.

Data sharing can lead to bespoke financial services

Banks and fintechs can also create robust pathways for data sharing among institutions. Advanced analytics can deepen our understanding of customer needs and preferences, enabling institutions to craft tailored financial solutions.

This comprehensive approach would elevate customer satisfaction and open doors for marginalised communities.

These insights were central to discussions during a roundtable at the Africa Financial Summit – AFIS 2024 in Casablanca, titled ‘Untapped Opportunities: Expanding Financial Services to Africa’s Fragile Market’.